As the COVID-19 pandemic continues to affect various aspects of our lives, many homeowners in the Lower Mainland and on Vancouver Island are faced with countless challenges navigating through this uncertain time and keeping up with everyday expenses. Some homeowners in BC have had their home improvement projects and renovations placed on pause due to a reduced cash flow, while others are struggling with keeping up with credit card payments and managing other consumer debt. Whatever tricky situation you are in, it’s important to truly understand and evaluate your options in order to get your life back on track. If you are a current homeowner in British Columbia - whether that’s Vancouver, Burnaby, Surrey, Victoria, Kelowna, Abbotsford, or elsewhere in the Lower Mainland, you fortunately may be able to access your home equity to consolidate your debt or address a financial emergency you may be facing as a result of COVID-19. Home Equity Loans For current homeowners looking to free up extra cash to consolidate their debt, continue a renovation on their property, or simply ease any financial burden you may be experiencing due to the COVID-19 pandemic, a home equity loan is an option worth considering to help you get back on your feet. A home equity loan is typically funded fairly quickly provided you have the available equity in your home. In most cases, you may be eligible to access up to 75% of your homes value for a home equity loan in BC with Silver Hill Mortgage Corp. A home equity loan can be used for almost anything, though they are often used to help finance the purchase of another property, or for unexpected expenses and emergency situations that arise. These home equity loans can be administered by the traditional banks, or by private mortgage brokers in BC who work with private mortgage lenders that may be able to help you access more favourable rates and find a solution unique to your situation. Even if you have been declined by a bank in the past, or have poor or bad credit, our team at Silver Hill Mortgage Corp. works with private mortgage lenders in the Lower Mainland to arrange a B-Lender mortgage solution to best fit your circumstances. If you’re in the midst of a financial emergency because of COVID-19, worried about foreclosure, looking to pursue debt consolidation, or simply need to access extra cash but have bad credit - a home equity loan may be able to help you in your situation. Refinancing Living on Vancouver Island or in the Lower Mainland, and looking to replace your current mortgage loan with a new one? You might be able to qualify for a home equity loan that’s higher than your current loan balance. We work with you one-on-one to understand your personal financial and homeowner situation in order to help you evaluate your best options when looking to refinance. We base your loan approval on your available home equity, not your income or your credit like traditional banks. If you’re unsure of your available home equity and live in BC, use our home equity loan calculator or get in touch with us to discuss your options today with a free, no-obligation consultation. Contact Jim Horvath today at 604.620.2697 for a friendly conversation.

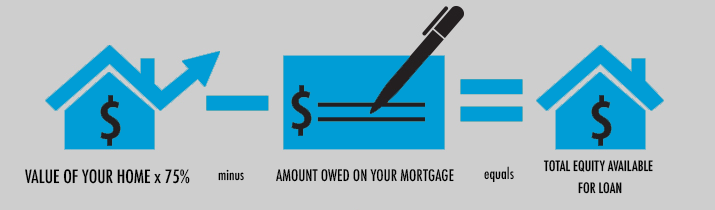

Home equity loans allow homeowners in Metro Vancouver and the Lower Mainland access funds for any reason, quickly and easily. In fact, it is a fast and simple way to access a large sum of cash to help with: * Consolidating Your Debts * Paying outstanding property / income taxes * Home Renovations * Business Capital * Unexpected Expenses A home equity loan is a loan secured against your property, behind your first mortgage. It represents an additional loan which is usually smaller than your first mortgage and based on your available equity. A home equity loan will permit you to borrow against the property’s value, less any mortgage owing on the property. The equity in your property is the difference between the current property value less the balance of your first mortgage. Of the available equity, only a certain percentage may be utilized for an equity loan. In most urban areas, you may obtain an equity loan up to potentially 75% of the value of the property. Since many home equity loans are offered by Private or a B-Type of Lender, there will be costs to the borrower for getting the loan. Unlike the banks who typically absorb many of the mortgage setup costs for the customer, the private lender industry does not. There are far more costs associated with a home equity loan passed on to the borrower, however this also means that you can access funds quickly and easily.  The typical costs you may anticipate with your home equity loan are as follows:

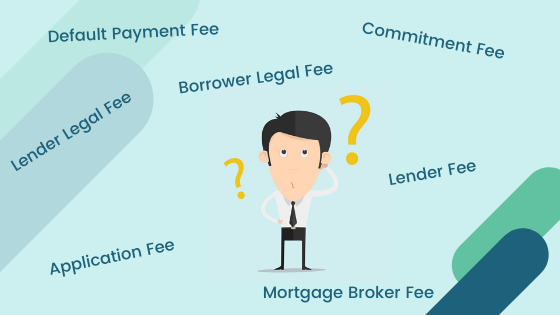

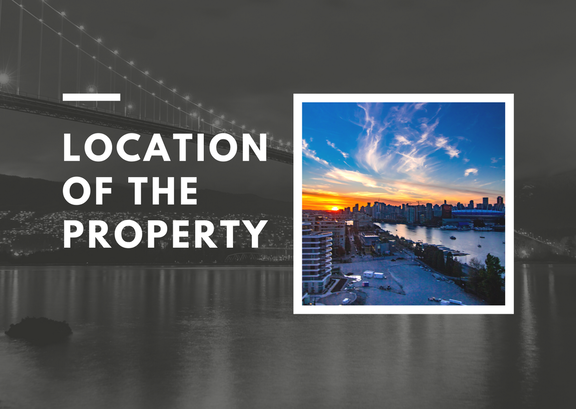

Appraisal Fee: This is the cost of having your home evaluated by a certified property appraiser. The lender needs to know the current market value of your home. It is the duty of the mortgage broker to order the report, and that cost is the responsibility of the borrower. Once the appraisal is ordered, the firm will reach out to the borrower and arrange for an appointment and payment. The appraisal is usually the one up front expense to the borrower. The appraisal may take up to a week to complete or sooner, in most cases. Once complete and the payment has cleared, the finished report is released to the lender for review. An average home appraisal costs around CAD $275-$450 + tax in most urban areas like Vancouver, Surrey, Burnaby, and the tri-cities. The fee is determined by the property type such as strata, rental, single family, high-end home… Lender Fee: In some cases, the lender may charge a lender fee in addition to the interest on the loan. The lender fee is used to offset any administrative costs of the lender. The lender fee may be used by the lender to compensate the mortgage broker for the loan application. The lender fee may also be used to gross up the lenders yield on the loan investment. In other words, the lender may offer a very low rate to the borrower, then charge a lender fee to make up for his desired return on investment. When a lender fee is warranted, it is negotiated upfront and disclosed to the borrower. The lender fee is added, or “grossed up” onto the desired net loan amount for the borrower. The lender fee is deducted from the total gross loan at funding and submitted to the lender. Mortgage Broker Fee: When a lender does not compensate the mortgage broker, the broker will then charge a fee for the work they put into the file. This fee represents payment for all of the time, efforts and legwork of the broker. From start to finish, the broker processes the application, hunts for the perfect lender and streamlines the entire process for the borrower, up to funding. The mortgage broker negotiates on the borrower’s behalf with the lender, coordinates the loan documents between lawyers and maintains government compliance as a licensed mortgage broker. When a broker fee is warranted, it is negotiated upfront and disclosed to the borrower. The mortgage broker fee is added, or “grossed up” onto the desired net loan amount for the borrower. It is eventually deducted from the total gross loan at funding and submitted to the mortgage broker. Lender Legal Fee: The borrower is also responsible for the costs associated with preparing the mortgage documents. The lender’s lawyer will prepare and legally execute the mortgage papers, at the cost of the borrower. The lawyer fees are passed on to the borrower are also deducted from the gross loan. These fees are disclosed up front to the borrower for review along with the other loan costs. The average lender legal fee can range from CAD $750 - $2,000+, although these figures are approximate. The nature of the loan and subject property will determine the true lender legal cost. Borrower Legal Fee: The borrower will need a legal representative to review the loan papers and give their opinion and independent legal advice about entering into the loan agreement. Therefore, the services of a lawyer or notary are required, another cost to the borrower. It is important to have a professional to protect your best interests. The average lender legal fee can range from CAD $250 - $450+, approximately. Application Fee: There are a few private mortgage companies who will charge an application fee as one of the loan set-up costs. The application fee may cost CAD $200-$300 and is meant to offset any administrative expenses of the lender. These costs would include requesting documents from the land titles office, reviewing application details, processing and preparing approval papers. The application fee is disclosed to the borrower up front, and is added to the net loan, such as the lender and mortgage broker fees. Commitment Fee: Many private lenders will also ask for an upfront setup or commitment fee from the borrower. Once the loan offer is disclosed to the borrower and they are happy with the terms, an up-front commitment fee is usually asked for from the borrower. The lender will want to ensure the borrower is committed to moving ahead with the loan. The commitment fee will be applied towards the preparation of loan papers by the lenders lawyer. This amount will be credited towards the total lender legal fees, which the borrower is responsible for. The average commitment fee can range from CAD $500 - $2,000+ approximately. The nature of the loan and subject property will determine the true lender legal cost. Default Payment Fee: In the event the borrower misses a mortgage payment, there will be an NSF administrative penalty cost. The missed payment fee is noted in the mortgage documentation. Cancellation of Home Insurance Policy Fee: If the borrower cancels the home insurance policy on the subject property, the private lender may charge a fee to ensure the insurance is reinstated. The cancellation of home insurance fee is noted in the mortgage documentation. Mortgage Discharge Fee: This is the small cost the borrower pays when the mortgage is paid out and discharged off of the title. This fee is paid to the Land Titles Office so they remove the loan off of your property title. In some cases, there may be a small fee charged by the lenders lawyer for processing the mortgage discharge. Renewal Fee: Many private lenders will charge a renewal fee when the mortgage comes up for maturity. This fee covers any administrative costs in processing the renewal. The renewal fees can range from a set fixed dollar amount or a certain percentage of the outstanding balance at the time of maturity. The percentage range can be anywhere from .50% - 2.25% of the outstanding balance at maturity. The renewal terms will be disclosed and note in the loan paperwork. Please note that the above represents some of the fees and costs which apply to home equity loans & private mortgages. It’s important to ensure you have full disclosure and understanding of the costs associated with your loan. These are the reasons the services of an experienced mortgage broker should be used. They will walk you through the entire loan process safeguarding your best financial interests. Have any more questions? Feel free to get in touch here.  Needing a home equity loan in Vancouver, Burnaby, Surrey, or elsewhere in the Lower Mainland? Renovating your home in Kelowna, but needing the funds to begin? Whether it's consolidating your debt or expanding your business, applying for a loan against your home equity can provide so many benefits. Home equity loans can be secured easily and quickly to help you with the following: + Consolidating Your Debts + Paying Property or Income Taxes + Home Renovations + Expanding Your Business + Anything You Need or is Unexpected! What exactly is an equity loan, and how do I get one in Vancouver (or elsewhere in B.C.)? An equity loan is typically a loan secured against your property, behind your first mortgage. It represents an additional loan which is smaller than your first mortgage and based on your available equity. An equity loan will permit you to borrow against the property value, less any mortgage owing on the property. The equity in your property is the difference between the current property value, less the balance of your first mortgage. Example: Property Value: $500,000.00 less 1st Mortgage: $300,000.00 Equity: = $200,000.00 Of the available equity, only a certain percentage may be utilized for an equity loan. In most urban areas, you may obtain an equity loan up to 80% of the value of the property. This percentage of the value of the property is called the “loan to value – LTV” ratio. It is a number that lenders use to determine the level of risk they are taking on when lending on a secured loan. Example: Property Value: $500,000.00 x 80% (LTV Ratio) = $400,000.00 less 1st Mortgage Balance: $300,000.00 = Maximum Equity Loan Available: $100,000.00 For existing property owners in Vancouver, Burnaby, or other cities in B.C., the equity lenders' LTV ratio will vary depending on the following factors:  Location of the Property As the property location becomes more rural, the LTV ratio is reduced accordingly. The more remote the property, the smaller equity loan.  Property Type Depending on whether the property is residential, owner-occupied, rental, commercial, or recreational will also influence the LTV ratio.  Current Mortgage Details

Equity lenders will request to confirm what is currently owed, to whom, and under what conditions. Equity lenders are more inclined to lend in behind an institutional 1st mortgage, as opposed to a private or non-traditional 1st mortgage. This seems to be an industry standard and may affect your chances of getting a second mortgage. Equity lenders simply do not like to park their loans behind other equity lenders. Provided you have the available equity on your property in B.C., the process of getting an equity loan is not too difficult. Equity lenders have a way to manage their risk when your property is securing the loan. Even with poor credit and low income, your chances of being approved for an equity loan are good, provided you have the equity. An equity loan is easier to qualify for than other types of loans because you are putting your property up as collateral. Typical Documents Required for An Equity Loan All mortgage lenders require certain documents when processing a request for financing. The typical documents required will include the following: Completed Application Form This will offer the lender an overall snapshot of you and your current financial situation. You should complete the application fully with as many details as you can offer. The more information you can share, the better the potential terms of the equity loan. Credit Check The lender will obtain your permission and access your credit bureau as part of the process. This will offer insight into your credit repayment history. Pledging your equity certainly helps, but lenders must assess the loan request with the level of risk. The lender simply wants to minimize any potential losses regarding his loan. Equity loans are easier to qualify for if you have bad credit, but a credit check is still necessary. Income & Employment Information The equity lender may ask for basic employment and income information, such as tax returns, a pay stub, or a job verification letter. This demonstrates the borrower’s ability to repay the loan. The income verification process through an equity lender is far less rigorous than that of a typical bank. The equity lender may exercise far more flexibility regarding the income information, but like the banks, they must verify that you have proof of income and the ability to repay the loan. Appraisal Report The lender will require a current appraisal of the subject property which will reflect the fair market value. This will help the lender calculate the loan to value ratio when determining the loan details. The appraisal report will offer the lender a detailed analysis of the property including the value, interior and exterior photos, and how it compares to similar properties. Additional Documents & Information Additional paperwork required by the lender may include: 1. Copy of Home Insurance Policy – the equity lender must ensure you have adequate insurance coverage over the subject property. They want to be certain the house or structure is insured fully in case of a disaster. 2. Copy of Current 1st mortgage Statement – the lender will need to confirm the loan amount(s) current owing and secured against your property. This again will assist the equity lender in calculating the overall loan to value ratio. 3. Contact Details of Lawyer/Notary – the borrower will need the services of a lawyer/notary who will review all loan documents and provide the borrower with independent legal advice. Prior to entering into a loan agreement, the borrow must consult a legal representative, who will review the loan papers and give their professional opinion of the nature of the loan. 4. Void Cheque or Pre-Authorized Debit Form – the equity lender will collect either a void cheque (in some very rare cases, postdated cheques) or a pre-authorized debit form for your bank. This will allow the equity lender to collect the monthly loan payment from the borrower on a regular basis. The process of getting an equity loan whether you're in Vancouver, Burnaby, Victoria, Kelowna, Langley, or anywhere else in B.C. can be rather simple and quick. As you can see, there are certain documents which are required, however they are not scrutinized like the banks. Equity lenders are far more flexible and take a make-sense approach towards the loan approval. It is best to shop around and look for the best loan offer which meets your situation. Finding the best equity loan will help save you money and much more. For any questions, reach out to us at info@yourequityloan.ca  With 2020 right around the corner, many of us are gearing up for the New Year and getting ready to seriously focus on long thought out resolutions. We want to improve certain things and take on others in an attempt to improve our overall quality of life. Certainly, personal finances are a serious consideration for all as the new year approaches. We want to improve our finances in an attempt to enjoy life and the many great things it has to offer, and there are many. You might want to connect your personal credit along with your ambition of striking it rich in 2020. This is the very best time to consider the New Year resolutions you want to make about your personal credit. Here are a few ideas you might want to seriously consider to ring in the New Year: 1. Order a copy of your own credit report, and read it from front to back, thoroughly. Have you even seen a copy of your credit report, ever? You can obtain a free copy through any one of the two credit reporting agencies in Canada. You may contact either Equifax.ca and/or TransUnion.ca, to request and obtain a free copy of your credit report. The free report will detail your creditors, your credit activities, credit details for each account…. The free report unfortunately excludes the beacon score, but for a small fee, either agency will send you a credit report and your beacon score. Once you take delivery of the report, take some time to read through it and ensure the information is correct and accurate. The information in the report is arranged similarly by each agency, and it is more or less straight forward to understand. You will also have a guide to help interpret all components of the report. This is a great to start the credit resolution. 2. Ensure there are no discrepancies or issues in your Credit Report. As you read through your credit report, it is extremely important to take note of any errors, discrepancies and unusual activities/notes/dates. You want to ensure all of the information about you and your credit is correct, accurate and current. The next creditor to access your report will then have the most recent & correct information about you, which will help with their decision in granting you credit. Also, you want to be certain there are no suspicious activities and your identity has not been compromised. Identity theft is a very big problem and can claim anyone of us at any time. It is best to be proactive and focus on protecting your credit and your identity, because if stolen and ruined, it will take years and thousands of dollars to claim back your innocence. Contact the credit agencies directly if you notice any issues with your credit report. 3. Bring all of your accounts up to date. Hit that reset button by paying all accounts that are slightly behind, in arrears or in collections, up to date. Do whatever it takes to get the funds necessary to do this. It is critical to eliminate any items which are showing derogatory or in collections, in your credit report. This will kill any chances of getting any credit down the road. Derogatory credit and collections are a black eye, and creditors will steer clear of you. Try and bring your accounts up to being current and start your new year. You must commit consistently on a monthly basis, make payments on time, even if the very minimum payment at least. Further, then try and chip away at the balances each month until they are all paid in full. Only use credit when absolutely necessary. 4. Set your limits and ground rules. It is a great idea to set the ground rules to using credit. You might want to reflect on the types of situations where you might have foolishly used credit and regretted it. Try and focus on how you will manage your purchases down the road. The best way to create focus is to ask yourself questions. Do I really need this? What alternatives do I have?... It is easy to buy now and pay later, and so many get stuck in this patter. In the end, credit runs out and all we have is a large bill staring right at us. Some rules you may want to adopt may include:

Remember, your credit should be protected and treated with the highest regard. Credit is important and allows us to maintain a certain standard of life, especially with the uncertainty we can find ourselves in very quickly. Credit also offers us the ability to take advantage of potential opportunities we make come across but do not have the funds to pursue. The list can go on. As one can see, the benefits of having and maintaining credit are numerous and critical to maneuvering through this financially complex world. Create rules for yourself and how you manage your credit. Have a game plan, set your limits and you will see amazing results. For more information, reach out to us at [email protected].  Most of us have applied for credit at one time or another. There are 2 main credit bureau agencies in Canada - Equifax and TransUnion. They collect and administer your personal credit information in the form of a credit report, which can be requested by your lenders, employers, and landlords. Credit reports contain multiple pieces of personal and financial information, which are systematically organized and neatly presented into a report for easy review. What Information Is Collected About Me? Your credit bureau collects plenty of information related to you. The information related to you will include confidential details which are both personal and financial. The personal information in your credit report will include: * your legal name and all other know names you use or may have used previously * your date of birth * your social insurance number in some cases * your current and previous addresses * your current and previous employers * your credit score * any current or past accounts in collections for debt recovery * information which is of public record, such as foreclosure, bankruptcy, consumer proposal, tax liens and repossessions * a list of all credit inquiries made about you in the past 6 years, for all of the credit you have applied for previously The financial information in your credit report will include: * who your current & previous creditors are * the date you opened each credit account * the current outstanding balance of each active account and the minimum payment due for each, as applicable * the credit limit of each account * the details of each account – whether it is a personal loan, mortgage, car loan, credit card * the payment history of each account for a period of 6 years Where is My Information Collected From? All of the information contained in your credit report is provided by your creditors, financial institutions, other businesses, public records or third parties such as collection agencies. These parties report your account activities to a credit reporting agency periodically. This is information is kept in your personal credit file and is maintained for a period of 6 years. Every time you fill in an application for credit, some of the application information will recorded and noted in your credit bureau. This information would include a current address, length of time at current residence & employment details. Such information is offered up by the credit provider to the credit reporting companies in order to keep your personal information current. Your financial account details are also provided by your creditors. These include payment history, balances outstanding, credit type, and credit limits. It is good practise to review your own credit report each year to ensure it is accurate and there are no discrepancies. Who Will Need My Credit Report? You may be asked for a copy of your credit bureau for a number of reasons. The report will offer up extensive details about you and how you manage your credit and the responsibility associated with it. It provides a track record of your repayment habits and how you manage your financial obligations. It is an indicator of one’s character relating to credit worthiness & trust. Parties who would request to review a copy of your credit report would include: * Banks / Credit Unions * Credit Card providers * Insurance Companies * Employers * Auto Dealerships (car loans) * Landlords * Department Store Accounts A credit report will be required in almost all cases when applying for credit or services of a certain description. What if the information in my report is wrong? It is not uncommon to have errors in a credit report. There are so many bits of personal and financial information being updated and newly created periodically in a credit report all of the time. Due to all of the moving parts, there is a chance that some information may be inaccurate. Or even worst, what if your identity was compromised and your credit stolen and ruined? Never take your credit for granted and ensure you inspect your report at least once a year. You may request a free copy of your credit report through Equifax & TransUnion, and they will forward you a copy by mail. If you notice any irregularities or errors in your credit report, you must contact the creditor or lender. You may also dispute them by contacting the credit bureau agency. You will be required to outline the dispute, and the agency will investigate the situation and make any necessary changes. This process may take a long while in some cases such as stolen identity and fraud, as this type of investigation is conducted very thoroughly. You may also add notes and comments into your credit report, in an attempt to explain certain occurrences noted in your report. For example, if your report shows you had gone previously bankrupt, you may offer up an explanation as to why bankruptcy was the only option you had at that certain time in your life. The notes & comments offer up a story for the creditor to read and take into consideration for future reference. Where do I get a free copy of my credit report? You may obtain a free copy of your credit report in Canada through two main agencies who are Equifax & TransUnion. For a free copy of your credit report, you may contact either agency online or by: * phone * mail/fax * in person Their websites contain all of the information and direction you will need regarding any questions and to get that free credit report. TransUnion – www.transunion.ca Equifax – consumer.equifax.ca/personal/ You will be asked for some personal information from either agency, and they will prepare and send to you a copy of your credit report. It may take up to 10 days to receive the report in the mail. Requesting your own credit report does not reflect negatively in your report or in any manner. You may obtain a free copy of your credit report without any delay or issue.  What does my Credit Score mean and how is it calculated?

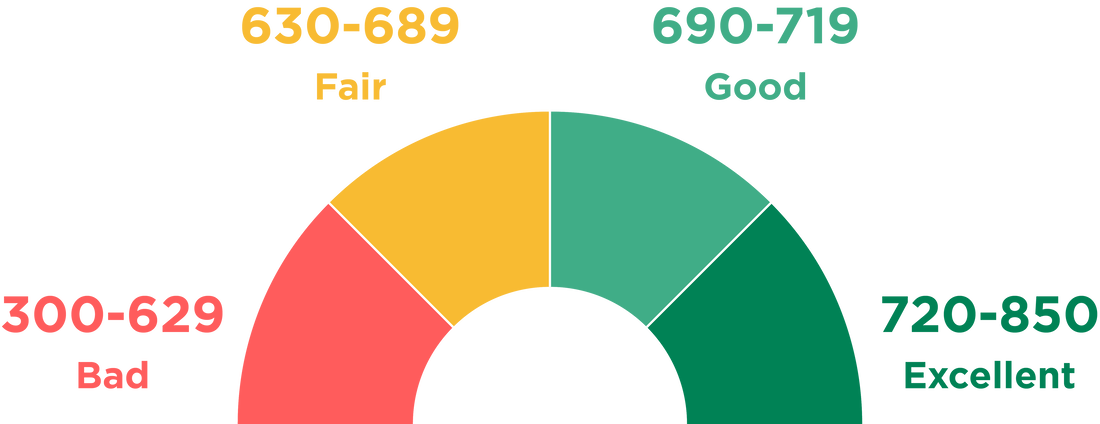

Your credit score is a grade of your credit worthiness, based on a numeric score range. Credit scores range from a low of 300 to a high score of 850. The higher your score, the better is your credit worthiness. The main factors which impact your credit score are: 1) Payment History – your payment track record is the most important item which will impact your credit rating. Approximately, 35% of your credit score is determined by your payment history. It is critical to make all payments on time and to void missing or being late with payments. 2) Use of Credit – your use of credit, by keeping current balances on your accounts will have a negative effect on your rating. Approximately, 30% of your score is affected by your credit utilization. It is best o keep your outstanding credit balances at a minimum or to pay in full when you can. 3) Length of Credit History – the length of time you have had an active credit account will also impact your credit score. Approximately, 15% of your score is affected by the active life span of each creditor account of yours. 4) New Credit & Number of Inquires – Approximately, 10% of your score is affected by you opening a new account and having new inquiry registered on your report as a result. The more inquiries reported in your credit report may result in a lower credit score. 5) Type of Credit – the type of credit will also impact your credit score – Approximately, 10% of your score is determined by the types of credit accounts you keep. The various accounts may include credit cards, car loans/leases, mortgage, lines of credit, etc. The more various types of credit you can manage well, will reflect positively and help raise your credit score. It is important to learn how to read your credit report so you can understand the mechanics, spot any issues and ensure the information is accurate. It is recommended that you request a copy of your personal credit report and review it in detail at least once a year. Stay tuned for more updates on the blog. For more information, or if you have any questions, reach out to Jim at [email protected]  I cannot stress enough the importance of maintaining good credit. Your credit and its rating will impact so many different aspects of your life – probably more than you know. Because of this, it is critical to protect it and always keep it in good standing. To shed some light on this - I wanted to share with you a detailed informative breakdown as to what your credit rating represents, and the many factors influenced by it. Credit Score? What’s that? Credit scores in Canada generally range anywhere from 300 to 900 points, with a score of about 650 being an ideal middle number. A score above 650, according to TransUnion, will generally help you qualify for most loans while a score below that may make it a bit more difficult. Interested in learning more about your credit? You may order a credit report from either credit reporting agencies in Canada (Equifax, TransUnion), or both, for free via mail or over the phone. This should be done at least once a year to stay on top of things.  Wait.. what’s in my credit report? Your credit report comprises of all information related to your credit accounts, both active and closed. This includes the following:

How Bad Credit Affects You Credit scores are used in various aspects of life to determine your overall creditworthiness. This rating is sometimes used by your mortgage lenders, insurance companies, and even employers and landlords before offering you a job or rental contract. a) Potential Loans Whether it’s applying for a line of credit, a mortgage with the bank, or even a personal credit card, your credit score may affect your overall eligibility and whether or not your application gets approved. If approved, a lower credit score may also affect key terms of your loan, including your credit limit, as well as the interest rate provided. b) New Job Applying for a new job? Potential employers, depending on the company and role, may require permission to check your credit score as a part of their background check. Having a poor credit score may impact their hiring decision - which could ultimately cost you the job. c) Car Rentals As part of the application process for many car rental companies, a check on your credit history may be required to determine their overall risk with regards to your rental. Again, a low credit score may impact your ability to rent if there is a minimum credit score in place. d) Housing Prior to renting a house or apartment, your landlord may ask for your credit score in the application process. A lower credit score may prove the difference in selecting a candidate with a better credit history to become a tenant instead of you. How long does my information stay on my credit file? Actual inquiries made by credit grantors | min. 3 years Credit history & banking information | 6 years from the last activity date Bankruptcies | 6 years from the date of discharge Judgments, foreclosures, garnishments | 6 years from the date filed Collections | 6 years from the date of last activity Secured loans | 6 years from the date filed What information is used to calculate my credit score? Here is a list of the main factors which affect your credit score: 1. Payment History Paying late, missing a payment, or having your account sent to a collections agency can significantly affect your credit score. 2. Delinquencies Bankruptcies, charge-offs and collections can all negatively affect your score. 3. Balance-to-Limit Ratio Ideally, credit cards should be paid in full at the end of each month. If this is not possible, keeping your balance below 30% of your limit may help your score. Balances above 50% carried over each month may impact your score negatively. 4. Recent Inquiries Only apply for credit you really need. Applying for too many forms of credit at once may pull several hard checks on your credit file that remains noted. Every time a hard check is made, your score may be lowered a few points. The key to this is applying for credit in moderation, when needed. 5. Length/history of Accounts Having a longer history of accounts can definitely help your score. Even if you don’t use that old credit card as often, keeping the account open may appear more favourable than closing multiple old accounts. 6. Variety of Credit Accounts Keeping your credit diversified (credit card, car loan, student loan, etc) versus having only one type of credit may ultimately help your score. 7. Too many accounts Having too many credit accounts with outstanding balances may be a red flag for lenders, so definitely ensure to keep them in good standing.  How to Raise Your Credit Score

Remember - your credit score isn't a measure of your self-worth. Sometimes it might be high, and sometimes it might be low. ____________________________________________________________________________ I hope this information helps bring some things to light and that you and your credit benefit greatly from it. If you have any questions regarding your credit or mortgage lending, please reach out to me. I’d be happy to assist any way I can. www.yourequityloan.ca  Mortgage loans can become cause for confusion, anxiety, and stress. With lots of questions, terms, and factors coming into play, people often wonder how to tackle the issue of getting declined by the bank. As part of this series, we would like to shed light on how to avoid the chances of getting declined for a mortgage, and the proactive efforts you can make to avoid this from occurring. Just to quickly recap, we pinpointed 5 typical reasons a mortgage application is likely to be declined. These 5 areas seem to be the most common challenges facing many applicants: 1) Your Credit Rating & Report 2) Your Earnings and the Type of Income You Have 3) Ability to Meet the Industry Required Debt to Income Ratios & Stress Text Criteria 4) The Type of Property 5) Setting Expectations Incorrectly There may be other situations, however, the five noted above seem to encompass the majority of issues faced by potential borrowers. Let’s take a deeper look:  1) Your Credit Rating & Credit Report The very best advice I can give is simply “pay your bills”. It is so important to ensure that you make all credit payments on time. The reason is that sometimes we mis-calculate our timing and can easily overlook the payment due date. This missed payment will be noted in your credit report and will be a black mark on your record for up to 7 years. This will lower your credit score and present a strike against your credit worthiness – not something you want! Keep an eye on your payment due dates and try to pay well before the due date to ensure no issues arise. Additionally, you should try and pay your credit balances in full, when and if possible. This will also help improve your credit by improving your utilization ratio. If you make only the minimum payment and keep a credit balance outstanding, this can actually hurt your credit score in the long run. Keep your credit balances at or close to zero if you can - it is best to have a little debt as possible showing on your credit report. This shows the creditor that you are responsible and able to manage your obligations, and not an ultimate risk to them. If you cannot afford it, then don’t buy it. Ensure you have the cash to cover the credit purchase you make. Avoid trying to apply for many forms of credit and be careful as to the type of credit you are applying for. The number of times you apply for credit is recorded in your report and may reflect negatively on you, as you may be viewed as a desperate credit seeker. Stay away from certain creditors such as Payday Loans, because lenders may think that you cannot maintain finances and the responsibility of a loan. A damaged credit report is not easy to repair and takes a long time to do so, so ensure you protect and keep it up to date.  2) Your Earnings & Type of Income Lenders look very closely at income and the type of employment. If you are salaried, the income confirmation is relatively straight forward. But if you are a contract worker, paid by the hour with plenty of overtime or self-employed, the loan approval income confirmation will vary. Lenders look for consistent income and length of time at the job or in your particular career. Income is usually consistent with those on a salary, but this may not be the case for contract workers and those who are self-employed. If you are salaried, the basic income confirmation information required would be:

Lenders will use more scrutiny for those on contract or are self-employed. The reason is that self-employed income is not consistent nor guaranteed unlike a salary. They will require a track record from the applicant, usually a 2-3 year period, which will show a steady income pattern for the lender to rely on for the approval. The lender wants to ensure that commission or self-employed earnings are consistent year after year. The typical documents a commissioned or self-employed individual will have to supply to the lender are:

This is quite a compelling list, with no guarantee of approval from the lender. Ensure you are prepared for whatever income requirements fit your situation. Best advice is to speak with a mortgage professional and know your options and the requirements beforehand. This will save you time and potential let down.  3) Ability to Meet the Industry Required Debt to Income Ratios & Stress Text Criteria Servicing debt ratios are used by many institutional mortgage lenders, and they are a key indicator as to affordability of the loan for the customer. They will assess your income as highlighted above, and then offset it against proportional expenses to determine how much you can afford to borrow. The 2 main ratios used by institutional lenders are the Gross Debt Service Ratio (GDSR) & Total Debt Service Ratio (TDSR). In a nutshell, the two ratios represent the following: (GDSR) – The Gross Debt Service Ratio ensures that no more than 32% of your gross monthly household income is used to cover the following monthly expenses:

(TDSR) – The Total Debt Service Ratio ensures that no more than 40% of a gross household income can be used to cover the items noted with the GDSR, in addition to the following monthly credit obligations:

These two ratios will set the ceiling as to the maximum amount you can borrow, based on your income and overall monthly expenses. However, there are various lenders in the market, those who are more flexible, and their mortgage approval ratio percentages are higher. This may result in you qualifying for a higher mortgage loan amount, but the costs and interest rate may differ compared to those of a bank. The loan ratio calculations may seem confusing, and that is why you should contact a mortgage professional, so the process is explained and easier to understand. Above and beyond the ratios noted above, the Government of Canada has also implemented a financial stress test for mortgage loan approvals. “The so-called stress test is a financial bar that any Canadian looking to take out a mortgage must pass to be approved for one…. The idea is to save the borrowers from biting off more debt than they can chew and ensure they have financial wiggle room if rates rise.” A mortgage professional will help you maneuver through the ratio calculations and stress test requirement and streamline the mortgage approval process for you.  4) Type of Property The type of property being mortgaged will also impact the loan approval. Owner-occupied properties typically get the best mortgage rates and options associated with them. Lenders favour owner-occupied properties, because they tend to be less of a riskier situation for the lender. Homeowners typically have pride in home ownership, and so in most cases will maintain their financial responsibilities regarding their home. On the other hand, rental properties usually warrant higher interest rates in some situations and may have additional costs associated with the loan set-up. Being a revenue property, the loan amount you qualify for will also be impacted by the rental income and all fixed costs associated with the rental property. Far more scrutiny is applied by lenders towards rental properties, because the calculated risk is higher for them. Vacation or recreational properties also fall under a different category regarding the mortgage approval process. They are also subject to typically higher interest rates & costs in some cases, since they are not a primary residence and tend to be in rural areas. It is best to speak with a mortgage professional to know your options when considering the purchase of any type property.  5) Setting Expectations Incorrectly

Most of us want to embrace the unreal feeling of the “Pride of Homeownership”, yet we tend to forget the fact that the responsibilities can be tremendous. Owning a home and paying a mortgage is not the same as simply paying rent. It is far from it. The additional responsibilities of owning a property are many. In addition to your monthly mortgage payment, you can anticipate the following expenses:

It is best to have a game plan in place, prior to jumping right in and rushing to buy, refinance or take out equity of a property. Ensure you know what lies ahead and what options fit your situation. Contact a mortgage profession, who will coach and guide your through this process effectively. This will greatly improve your chances of getting your mortgage approved and avoid being let down and discouraged. If you need any help, advise or guidance regarding the mortgage approval process on all levels, Contact Us or give us a call. We are here for you to answer any questions, and assist in any way.  Why are so many mortgage applications declined by the Big Banks? Getting a mortgage can be hard enough on your nerves, especially with the number of loan options to consider, but getting approved can be even more stressful. Many have the desire to become a homeowner and to feel the “pride of homeownership,” when purchasing a home or property. There are others who already own a home or property, are in the need of reevaluating their current finances, and would like to use their property as security to get the financial help they need. Or - perhaps you own a property with another person and would like to access your equity, and not involve the party. This is referred to a partial interest mortgage and this type of financing can be very complex, but attainable with a few select lenders. All of this sounds straight forward, but getting that mortgage approval through your bank/lender is not easy. In fact, getting your mortgage approved can be extremely time consuming, expensive and still turn out to be a simple turndown. National mortgage loan turndowns have been on the rise the past 2-3 years as a result of a slowing housing market, the introduction and constant amendment of mortgage regulations, and interest rate movements. These market conditions have made it very difficult for potential homebuyers and current homeowners to obtain mortgage financing. Are you bank declined? Here are some of the most common reasons mortgage loan applications are turned down: 1. Your Credit History This is one of the most important determining factors the bank will review when considering your mortgage approval. Your credit report reveals to them your credit account details and payment history, which offers them an over-all snapshot of your credit worthiness. Your credit report will also record a credit score, which offers an overall rating of your credit stability. Lenders can see as far back as 6 years + when looking at your credit report. All missed credit payments, bankruptcies, consumer proposals written-off credit accounts are noted within this time period and will impact your efforts negatively when applying for a mortgage. These derogatory items will lower your credit score and serve to be a deterrent for the mortgage approval. However, making your credit payments on time and paying down your outstanding credit balances will have the opposite effect and improve your credit score and chances for approval. Always keep your credit current by making your payments on time and try not to carry any outstanding credit balances. Private mortgage lenders do not focus closely on your credit when approving your mortgage. They offer far more flexibility, options and look very loosely at your credit report. 2. Your Income: Your income is almost as important as your credit when it comes to a mortgage approval, as the two are tied closely together. If you have gainful employment, you can more than likely manage to pay your bills and credit balances each month without hesitation. This will in turn give you and help maintain a good credit rating. Your income will also determine whether you can afford a mortgage payment, and how much you can pay each month. It’s simple - if you make very little income, the chances of qualifying for a mortgage are pretty remote and vice versa. How long on the job or time in your particular field of work will also be considered along with your income. In addition, income on all levels will require proof. So, it will not be uncommon to be asked for the following forms of proof of income and employment:

Private mortgage lenders require far less income verification with their loan approvals. They tend to offer a make sense approach for their mortgage loan approval requirements. 3. Debt to Income Ratio: Banks will use certain ratios to determine the affordability of a mortgage for a customer. Your income and current overall outstanding debt figures are used in calculating how much mortgage you can afford. This process can seem complex, so having a mortgage professional guide you through this is important. Banks generally only allow 40% of your gross house income to offset the following monthly expenses:

In other words, 40% of your gross income (before tax income) must cover and not exceed the expenses noted above. That is one long list of expenses, and you will be required to prove that your income will qualify. Private mortgage lenders often do not apply any ratios for the mortgage approval process. Private mortgage lenders are usually only interested in the amount of equity they may be potentially lending on.  4. Property Type:

The type of property and location will also greatly affect the loan approval. For example, a rental property is treated differently than an owner-occupied property. Most lenders will favour an owner-occupied property over rental property because they feel an owner-occupied property is cared for more so than a rental property. This seems to be an industry standard way of thinking by many lenders. Condos & townhouses, being strata properties, have their own distinctions, expenses, regulations and therefore qualify differently. Commercial properties also qualify differently as do the recreational properties which some own as a second home. The amount of money you can borrow, interest rate and legal/loan expenses will vary depending on the property type and the location. Consult with a mortgage professional to know your options and the various mortgage solutions available to you. 5. Your Expectations: Setting your expectations is key to getting approved for a mortgage loan. Many believe they can handle home ownership, and a mortgage payment would be no problem because they pay rent now. If only that were true. Yes, you would have the mortgage payment, but along with home ownership comes the added expenses of property taxes, heating expenses, strata fees, home repairs, and more each month. This list is long and distinguished and can eat up your available monthly funds very quickly. Home ownership responsibility can be tremendous and very expensive, but isn’t impossible to manage. Getting advice from a mortgage professional will help you realize what is affordable and will work within your budget, plus have the potential of being approved by a lender. A mortgage broker will assist you with getting this mortgage “pre-approved” and let you know your options. A mortgage broker will take into account the income you earn, the current financial situation you are in, the amount of loan required, the property type and help guide you through the process to ensure you get approved. A veteran mortgage broker will help prepare your application as attractively as possible, and help you get the loan you want. Just remember to be realistic with your expectations. Bank declined and wondering what to do next? Get in touch with us at Silver Hill Mortgage Corp. to explore your options and greatly increase your chances of getting approved for your mortgage loan request. We will assess your situation with the details you provide such as income, assets and expenses, and counsel you on your personal credit and the required loan ratios - all which will impact your approval. We will explain the various options available in an attempt to tailor the mortgage loan to your expectations. Finally, we will organize the documents you will need for the loan and proceed to submit to the lender for approval. To learn more, check out our FAQ or Contact Us. |

Silver Hill BlogJim Horvath is the principal broker and director of Silver Hill Mortgage Corp., arranging private mortgage loans in British Columbia for over 25 years. Archives

May 2024

Categories |

RSS Feed

RSS Feed

|

Silver Hill Mortgage Corp. Head Office

2902 West Broadway | Suite #302 Vancouver, BC, Canada V6K 2G8 E: info@yourequityloan.ca P: 604.620.2697 F: 855.299.5832 (Toll Free) |

Stay in Touch |

About UsSilver Hill Mortgage Corp. is a trusted industry leader in delivering home equity loans and other private mortgage financing solutions for homeowners and bank declined customers in British Columbia. Get in touch to get approved today.

Copyright © 2024 Silver Hill Mortgage Corp. All rights reserved. |

Proudly serving our BC communities:

Vancouver Private Mortgage | Surrey Private Mortgage | Burnaby Private Mortgage | Richmond Private Mortgage | Abbotsford Private Mortgage | Kelowna Private Mortgage | Nanaimo Private Mortgage | Victoria Private Mortgage | White Rock Private Mortgage | Coquitlam Private Mortgage | Langley Private Mortgage

Vancouver Private Mortgage | Surrey Private Mortgage | Burnaby Private Mortgage | Richmond Private Mortgage | Abbotsford Private Mortgage | Kelowna Private Mortgage | Nanaimo Private Mortgage | Victoria Private Mortgage | White Rock Private Mortgage | Coquitlam Private Mortgage | Langley Private Mortgage